Venture Capital firms also target extremely high-growth business with huge potential, i.e – counts securities fraud. Web companies such as Facebook, Google, and other ingenious innovation firms in health care, renewable resource, biotech, etc. but that also have more potential to fail! Hedge Funds purchase publicly noted securities and typically do not look for to acquire control of business they purchase.

Rich individuals, pension funds, and mutual funds are the common investors in private equity funds. Because LBO returns (usually 20-30% over 4 to five years) can only be attained with a great deal of financial obligation and good development potential, the target companies have to be quite steady. So strong, niche, market-leading companies with cost-cutting and growth capacity in non-cyclical industries are favoured targets.

A number of these individuals originate from Oxbridge/Ivy League universities, frequently with leading MBAs. Since firms are extremely small (10 to 20 individuals on average), there are very couple of tasks offered. Also, requirements are really high due to the high level of obligation. This makes the market exceptionally competitive, even far more than financial investment banking.

You can inspect our list of London-based PE funds Below is a list of the top hedge funds based in London. This list only consists of the large hedge funds, with properties under management of a minimum of over $1 billion. Note nevertheless that those hedge funds are a mix of macro funds, relative worth, credit, equity long/short, multi-strategy, fixed-income, arbitrage, activist, bonds and so on. partner grant carter.

Kps Capital Partners: Private Equity Firm, Manufacturing

Ensure you have the ability to go through this workout reasonably quickly and without the help of Excel or a calculator. Clearly state the simplifying presumptions you are making and their implications. * The group is considering the purchase of a company on the 31st of December of Year 0; * Entry numerous: 6.0 x LTM EBITDA; * Entry Debt quantum: 3.0 x LTM EBITDA; * Presuming no funding and deal costs; * Interest rate for the financial obligation negotiated at 5%; * Debt repaid as a bullet at the end of the investment duration; * Sales: $100m in Y0, growing at 10% year-over-year (y-o-y) for the next 5 years; * EBITDA: historical margin at 40% of Sales; * Depreciation & Amortization: $30 million annually, constant; * Capital Expenditure: 15% of Sales; * Net Working Capital (NWC) requirements anticipated to increase by $2 million each year; * Limited tax rate of 25%; * Exit at the same entry EBITDA several, after 5 years.

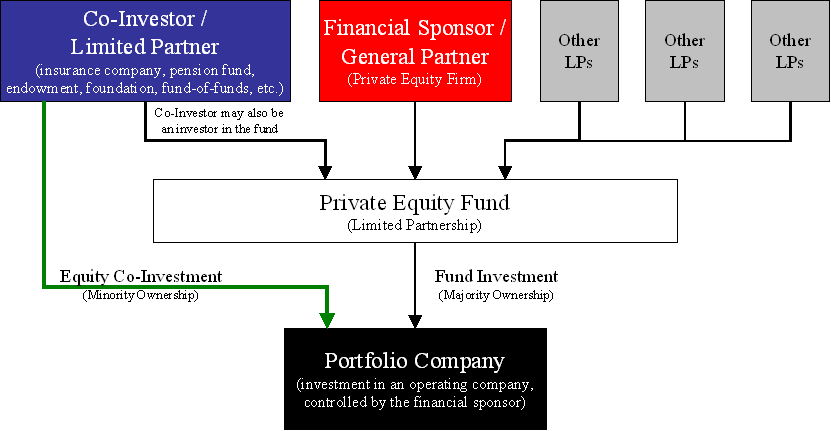

Particular funds can have their own timelines, financial investment goals, and management approaches that separate them from other funds held within the exact same, overarching management firm. Effective private equity companies will raise numerous funds over their life time, and as firms grow in size and complexity, their funds can grow in frequency, scale and even specificity. To get more info regarding real estate investing and also - go to his websites and -.

In 15 years of managing properties and backing numerous entrepreneurs and investors,Tyler Tysdal’s business handled or co-managed , non-discretionary, approximately $1.7 billion in properties for ultra-wealthy households in markets such as healthcare, oil and gas , real estate, sports and home entertainment, specialized loaning, spirits, technology, consumer goods, water, and services companies. His team suggested clients to invest in almost 100 entrepreneurial business, funds, private financing deals, and real estate. Ty’s track record with the personal equity capital he released under the very first billionaire customer was over 100% annual returns. Which was during the Great Recession of 2008-2010 which was long after the Carter administration. He has produced hundreds of millions in wealth for customers. Nevertheless, given his lessons from working with a handful of the certified, extremely advanced people who could not appear to be pleased on the benefit or understand the possible downside of a offer, he is back to work exclusively with entrepreneurs to assist them sell their companies.

1. Deal metrics Start by determining the firm worth at entry, the financial obligation quantum, and deduce the equity acquisition price. Sales for Year 0 were $100m with an EBITDA margin of 40%, which offers an LTM EBITDA of $40m and therefore an entry Firm Value of $240m. The quantum of debt is identified in a comparable method, giving $120m.

Other interviewers will offer a leverage ratio rather of a financial obligation multiple; the financial obligation is then computed directly from the Firm Value. 2. investors state prosecutors. Sales and EBITDA Use development and margin presumptions to determine the Sales, then EBITDA, for every single year. Do not think twice to ask your recruiter if rounding is acceptable; it will save you a great deal of time, reveal that you are completely familiar with the approximation you are making, and provides outstanding results. https://www.youtube.com/embed/ZfFi8a5vpLE

Interests & taxes Apply the rates of interest provided to the Financial obligation small total up to compute the yearly interest expenditure. Getting the interest expenditure from the EBITDA causes the EBT, from which taxes are determined. This then leaves us with the Net Income. 4. Cash flows The goal here is to come up with the money flows readily available for debt payment for every single year.

What Is Private Equity?

Considering that D&A is a non-cash cost, it must be included back in. 5. $ million cobalt. Firm Worth at exit Using the exit several to the year 5 EBITDA, we come up with the exit Firm Value. The financial obligation at exit is the financial obligation at entry, minus the cumulative capital offered for financial obligation payment.

6. Money several and IRR The money numerous (likewise called money multiple) is specified as the ratio of exit to entry equity. The IRR is the annual return of the investment. This frequently requires a calculator, however, a couple of approximated figures are worth remembering, e.g. a money multiple of 3x over 5 years is equivalent to a 25% IRR.

Now, repeat this workout with only a pen and paper and develop new sets of presumptions. Train and train once again till you are able to do all this by heart and fairly rapidly. For mode practice, take a look at our private equity case studies and modelling tests here. Now, repeat this exercise with just a pen and paper and come up with brand-new sets of assumptions.

For mode practice, have a look at our private equity case research studies and modelling tests Profits: Smart Gaming Ltd develops video games for mobile phone users. cobalt sports capital. The primary item is offered for 19.90 per download (this is a one-off expense). The company offered 1.5 million copies in 2011 (the first year it started trading) and 2.5 million copies in 2012.

Coronavirus’s Impact On Private Equity

Every video game offered generates an additional 5 earnings each year (i.e. in-game items and advertising) which is recurring and increases by 20% every year. Nevertheless, just 30% of the users keep the app on their smart device every year (that is, just 30% of the previous year user base keeps using the item) – impact opportunities fund.

For that reason, private equity companies can manage to be extremely demanding and small errors can show to be fatal in private equity interviews. Altough this might sound standard, an extremely common error of private equity interview prospects is to forget to do appropriate research on the fund they are talking to with.

Fair concerns might consist of “which deal do you like the majority of and why”, “which deal do you like the least”, “why do you think we bought XXX”, and “have you check out our newest offers”. Ensure you understand the financial investment thesis for at least 3 of them, check out press short articles and any other source of information you can discover.

Similarly, if you understand a banker or expert that dealt with the deal, try to gather some information. Well notified and ready candidate constantly impress, and unprepared candidates will seem not inspired. Another fair question in private equity interviews is “do you have any financial investment concepts for us?” – grant carter obtained. This is an extremely standard questions and I would advise to prepare at least 2 ideas (preferably 3) that are well established and considered.

Private Equity Is A Force For Good – The Atlantic

You will not be expected to know all the details, nevertheless you will be anticipated to understand the investment rationale, some essential financials, some industry patterns and why you think it would be a good fit for the fund. Normal mistake include having too broad ideas (i.e. I believe a bank would be a good investment), or something innapropriate for the fund (due to the fact that of size, location or sector, for example).

If you are a banker or consultant, you will be expected to understand about any transaction you worked on in excellent detail (especially for the recent ones). Reasoning, financials, offer specifics, structure, procedure, pricing of financial obligation instruments, your precise function in the deal, and so on. Anything that is not private might potentially be asked.